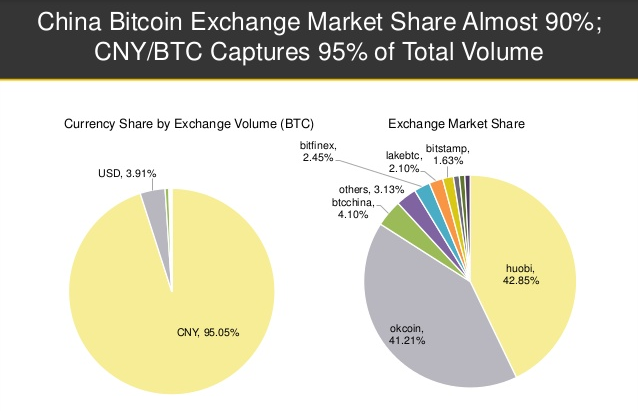

When VBTC as Vietnam’s first local Bitcoin trading floor was set to launch 5 years ago, the Bitcoin world was a very different one from the one which we know today. Mt. Gox was — with over 90% of the global trading volume — still dominating the global exchange landscape, even though the Chinese Exchanges led by a wide margin by BTCChina started to play a notable role as well from late 2013 on.

In the aftermath of the Mt. Gox collapse the global exchange landscape had to reorganize — much earlier and new- and upcoming platforms started to gain a serious foothold. While Western-based Exchanges such as Bitstamp, Kraken or later on GDAX (nowadays Coinbase Pro) all followed more or less a certain business ethics standard in regard to their offerings, many of their Asia-based counterparts — for better or worse — engaged pretty blatantly in various market manipulating activities in order to gain advantages over their competitors in an “anything-goes-cut-throat”-market.

It is undeniable, that many of the Western-based Exchanges — either due to regulatory pressure and or a generally different understanding of business ethics — are more “boring” in their offerings compared to many of their Asian counterparts. But “boring” in this sense means also more predictable — which is certainly in line with the expectations of many of Western-based investors compared to the “Wild West” that is the Exchange landscape in Asia.

While some of the tactics employed by a variety of Asian-based exchanges are simply deceiving — others are very close to circumstances which one could almost label as “stealing” from their customers.

Some of the most common schemes of which up- and coming cryptocurrency traders and investors should be aware of are listed below.

Wash trading: A common method for generating fake trading volume.

One of the most common practices among crypto exchanges in Asia. This practice appeared for the first time on a larger scale with the rise of various crypto exchange platforms in China in late 2013 which in order to attract customers reported outrageously blown up volume numbers.

“Washtrading” refers to the praxis that exchanges and/or related parties artificially increase the reported trading volume by repeatedly filling their own orders on the exchange — usually performed in a way, that no third party has the opportunity to fill these orders instead. At the same moment, the orders hit the book — they are immediately taken by the same and/or a related party.

Some exchanges take it a step further and even misreport directly their trade volume numbers without even going through the process to push the trade volume through the orderbook.

This practice is utilized in order to “fake” the appearance of a highly active, liquid marketplace in order to attract traders onto their platform.

Especially various illiquid Altcoins / ICO tokens have seen this practice adopted in order to cover up the fact that there is barely a market of willing buyers (or sellers) for them at all.

While there is no direct financial harm observable for traders on platforms that engage in wash trading — the lack of meaningful market data can bamboozle traders into taking positions in illiquid Altcoins/tokens without realizing that there is possibly no significant market activity available at all.

Fake trading volume method: Fake liquidity

While the previously described practice does not directly inflict financial harm on the exchange customers — the practice of “fake liquidity” in the orderbook very well does so.

Fake liquidity essentially is displayed orders in the orderbook, which you can not fill and/or disappear at the very moment you are trying to fill them.

This leads in the case of the customer conducting a market order to direct financial losses due to unexpected slippage. If for example, the customer is observing the bid side of the orderbook of an exchange deploying fake orders at 50 USD /LTC and in consequence decides to sell some Litecoin for 50 USD / LTC… — his order might just slip through until it hits the first “real orders” in the orderbook which might be several percentage points lower than the expected price point of 50 USD / LTC.

This leads to a direct financial loss of the customer deceived by sitting fake orders in the orderbook — to a benefit of the exchange operator and/or related parties who take part in this practice.

While not as prevalent as the practice of wash trading — various Asian-based “big name” exchanges having been reported over the past several years to regularly engage in deploying fake liquidity in their orderbooks to hide the fact that a) the exchange is not as liquid as claimed by the exchange management b) directly benefit from customers who fall into the “trap” of “fake liquidity” and unexpectedly get their orders executed far away from the initially expected market price from having a look at the orderbook.

Fake trading volume method: Front running

This is the practice of routing customer orders to trading desks either operated by the exchange itself or related parties in order to provide them a constant money-making edge in the market.

The exchange is utilizing its privileged access to its proprietary customer order flow in order to “front-run” their own customers and regularly “cheat” them out of a better order matching price.

For example, the exchange orderbook is displaying several asks at a price of 200 USD / Ethereum. The customer would like to purchase some Ethereum at the price of 200 USD and submits a market order — but before his market order gets executed his order gets routed to the trading desk operated by the exchange/related parties which executes a market buy order first at the price of 200 USD/Ethereum and immediately creates a new ask order with a higher ask price at e.g. 201 USD/Ethereum- which will be the order which the initial market buy order of the customer is going to match.

This creates a risk-free profit for the exchange / its collaborators — at the cost of the customer who constantly gets cheated out of a better matching price for his orders.

While this practice is not yet very prevalent in the cryptocurrency markets — with the current trend of the industry it is to be expected that these practices will find more widespread use soon to the disadvantage of common retail traders.

In the traditional financial world firms like Stock Brokerage Startup Robinhood build their major part of their business around selling customer order flow data of their prevalently millennial audience to large financial institutions and trading firms which pay obviously a very good amount of money for these kinds of data. It is access to risk-free trading profits after all.

Fake trading volume’s method: Stop hunting

Last but not least — Stop hunting.

While the previously described practices either “only” deceive exchange customers with false market data or cause them to have up to several percentage points worse execution prices — the practice of “stop hunting” regularly liquidates whole trading accounts/portfolios.

Naturally the “stop hunting” scheme is for the most part exclusively deployed on cryptocurrency exchanges which provide their customers with more or less “crazy” leverage on their trading positions — with the whole incentive scheme (due to a lack of legal enforcement against such practices) being set up in a way, which make it financially really attractive for the exchange to trade against its own customers.

To make this more understandable:

Let’s say an exchange customer wants to take a long position on Monero at 100 USD with a 20x leverage. He puts up a collateral of 1 BTC (6,400 USD). The customer holds, therefore, a long position of 1,280 XMR (Monero) with a value of 128,000 USD.

The liquidation price of the customer is therefore at about 95 USD / Monero (128,000 USD * 0,95 = 6,400 USD).

And the exchange knows that.

At this point, it becomes very attractive for the exchange to find ways to manipulate the market price of Monero on its books down to hit 95 USD / Monero — in order to liquidate the full position of the customer and pocket the collateral.

To avoid complete loss of their collateral traders usually, apply a stop-loss price to their orders far above their liquidation price. Let’s e.g. assume a trader has set a stop loss at about 20% of its collateral. In this case, his liquidation price would be at about 99 USD / Monero ( 128,000 USD * 0,99 ).

It is quite attractive/profitable in this case to push the price of Monero on the exchange somewhat down in order to trigger the stop loss of their customer.

At this point, there are very little countermeasures you can take against such shenanigans by the exchange besides managing your risk and position size accordingly. And of course, switch to providers with a reputation not to screw their customers over.

“The exchanges that have by far the highest volume per website visit, and which are likely engaging in significant volume faking are Coineal, Fatbtc, BW, BitMax, LBank, DOBI Exchange, Bit-Z, DigiFinex, Idcm, DragonEX, ZB, CoinTiger, IDAX, Bibox, CoinBene, BitForex, Bithumb, Negocie Coins, Liquid and OKEx.

On the other hand, Indodax, BX Thailand, Luno, CEX.IO, Zaif, and KuCoin do not appear to be faking any volume unless they are also engaging in faking traffic.

Over the past six months, the total reported trading volume was $1.96 trillion, of which only $272.5 billion appears to be real trading volume on non-volume faking exchanges.

About 86% of the trading volume looks to be fake with 65% of that total real volume originating on Binance and Bitfinex, both of which have virtually no regulatory oversight.

(Source: The Block)

Conclusion

Especially if you are new to the Crypto markets, you might want to make yourself familiar with these kinds of practices early on — before you lost a whole lot of money due to the questionable behavior of your exchange provider.

The mentioned Sylvain Ribes compiled a useful list of the legitimacy of various exchanges in this Twitter thread.

VBTC is Vietnam’s first Bitcoin Trading Floor (operating since 2014) — providing the lowest fee structure with various funding & withdrawal options to provide a seamless experience to our client base.

VBTC’s trading volume numbers and listed orders in the orderbook are 100% real. VBTC does not engage in any of the practices listed in this article.