TL;DR: The TON ecosystem is transitioning back toward the Gram brand, and BitcoinVN now supports higher instant swap limits for Gram (TON) assets, including USDT on the TON network. This article is not investment advice. Users should exercise extreme caution and conduct their own thorough due diligence before investing in cryptocurrency.

While the crypto markets overall remain under significant cyclical and structural pressure these days, one of the more widely utilized cryptocurrencies, TON – or as it is now known, Gram – continues to make moves to further entrench itself within the global crypto economy.

And while we remain generally highly skeptical of most crypto projects – and would urge even greater caution when it comes to investing actual money into them – it also cannot be ignored that Telegram founder Pavel Durov is one of the most impactful tech founders of the early 21st century.

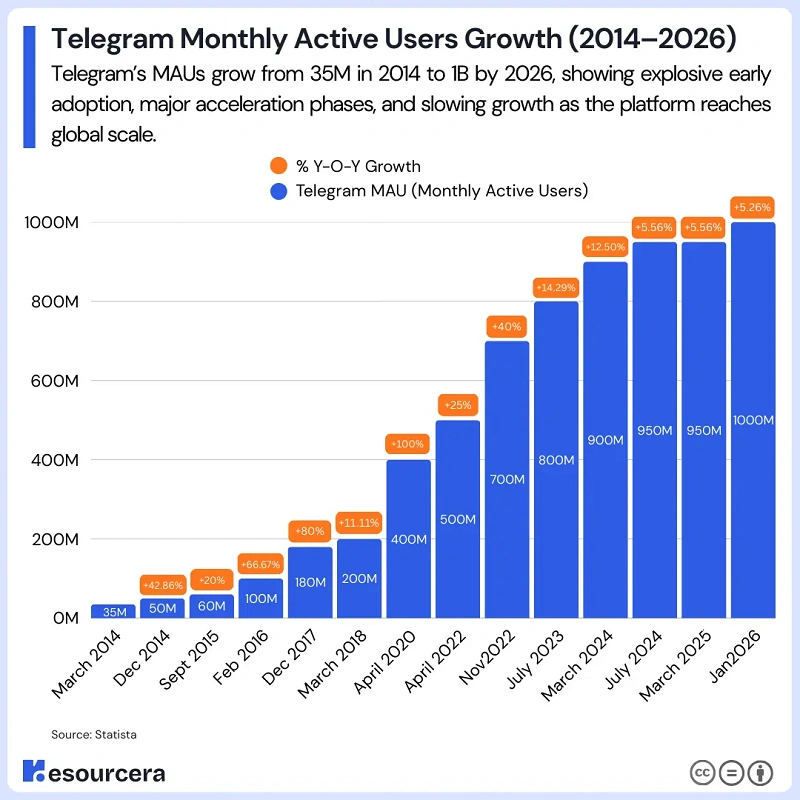

If you deliver an app with more than a billion monthly active users, then whatever your personal opinion of Durov or Telegram may be, those are still very noteworthy numbers – a level of distribution and service at scale that very few technology providers have ever been able to achieve.

While Gram (TON) is certainly a highly centralized cryptocurrency project – and makes less effort to bamboozle the public about it than many other pseudo-decentralized cryptocurrencies – this is still a caveat people should keep in mind when exposing themselves to Gram (TON).

It is essentially a token that lives and dies with the success of Telegram Messenger and its founder Pavel Durov. If Telegram continues to do well – and we currently do not have any particular reason to expect its demise in the near or medium term – then the project will likely remain active and alive.

Should that ever change, however, the outlook for Gram (TON) would obviously worsen fundamentally, and it could, like so many thousands of abandoned crypto projects before it, likely turn into another zombie project.

In other words, Gram (TON) carries a significant key-man risk – one that genuinely decentralized cryptocurrency projects simply do not have.

Price performance of Gram (TON)

Now, we are well aware that many people “interested in cryptocurrency” care very little about the underlying technology and instead focus almost exclusively on one question:

“Can I get rich with it? Will buying this thing make me a lot of money?”

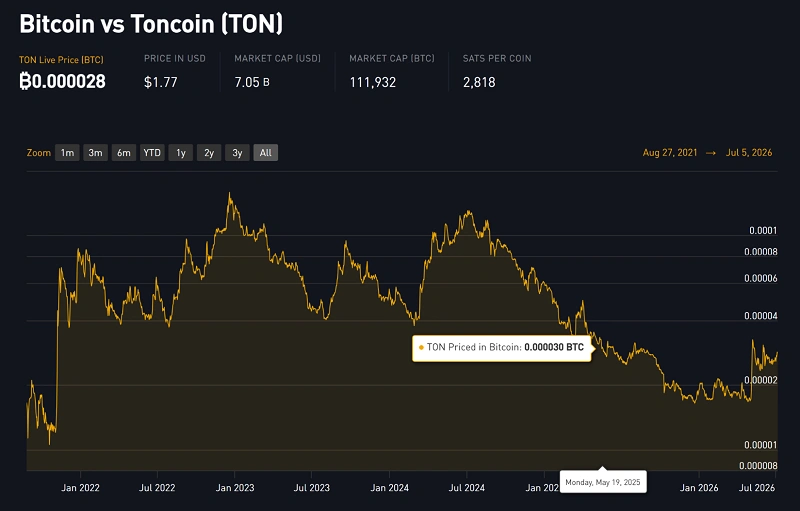

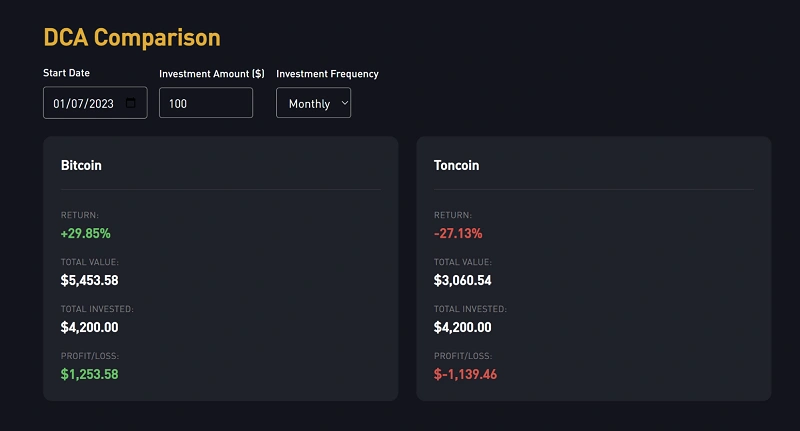

While we’re certainly not here to provide financial advice – and would in fact encourage you to reconsider an investment philosophy that ignores fundamentals in favour of hype-driven narratives (as such an approach often results in transferring your capital to more disciplined market participants) – let’s nevertheless take a look at the historical price performance of TON (Gram) compared with the industry’s benchmark asset, Bitcoin (BTC).

…and – as many people still like to measure their assets versus the “world reserve currency” USD (a broken yardstick in our opinion, but you can learn more about this in other places)…

Now, we have to admit that these numbers surprised us somewhat – and perhaps they should also give the Bitcoin community pause and prompt some serious reflection on how we arrived here. Once “Number Go Up” (NgU) became accepted as an almost inevitable law of nature, it arguably ceased to work. Strip away the extraordinary early-adoption years of the 2010s, and the investment picture of the 2020s suddenly looks far more sobering.

While price action should never be the primary criterion for evaluating an investment – and is, over a sufficiently long time horizon, largely a derivative of the strength of an asset’s underlying fundamentals – the fact that Bitcoin has essentially been “trading sideways” over much of the past half-decade should serve as an early warning sign.

If we do not put in the work to protect and strengthen Bitcoin’s fundamental value proposition, the market results will ultimately reflect that.

Our own observation is that genuine Bitcoin adoption – people holding their own keys and using Bitcoin directly, whether as a savings vehicle or a payment network – has progressed considerably more slowly than many enthusiasts of the 2010s had projected and anticipated.

That is not to suggest that optimizing for price at the expense of Bitcoin’s underlying value proposition is the correct response.

In fact, one could argue precisely the opposite. The increasing focus on “optimizing for price” through various paper wrappers around Bitcoin – financial products that Wall Street is more than happy to sell in effectively unlimited quantities to a steady supply of willing buyers – has arguably diverted attention away from building hard technology and protocol-adjacent infrastructure for end users, and toward ever more complex forms of financial engineering that bury actual Bitcoin beneath layers of claims, custodians and counterparties.

As for Gram (TON) itself:

Generally, in our view, it makes very limited financial sense to allocate longer-term savings into assets with large “minted-out-of-thin-air” pre-allocation overhangs, where early institutional investors eventually need to exit in order to generate returns for their fund LPs.

In simple terms: you are paying market prices for something that others received either for free or for pennies on the dollar – and which they now need to monetize in order to demonstrate to their investors that their capital was allocated successfully.

Even more so, tokens generally do not provide the same level of investor rights, legal protections, or governance mechanisms that shareholders in listed companies typically enjoy.

Combined with the severe key-man risk outlined above – namely, the risk that Telegram declines in relevance or strategically withdraws support from Gram (TON) – this makes Gram (TON) a questionable vehicle for ordinary savers looking to allocate long-term capital.

With that said, we are not your financial advisor and you are of course free to ignore such cautionary disclaimers at your own discretion.

If you are more of a short-term speculator – not a lifestyle we endorse, but one we understand is nevertheless quite common these days – Gram (TON) at least has serious backing from Telegram and its founder, who has remained committed to the project through years of legal challenges.

That does not necessarily make it a great investment. But compared with 99% of other “crypto projects” that essentially take your money and run while dressing it up in prosaic, verbose language about “handing it back to the community”, Gram is perhaps one of only a small handful of coins that has seen actual real-world usage beyond pure price speculation.

If all of this sounds like far too much work – and you have no desire to become a part-time analyst, spending countless hours reading charts, digging through on-chain data, and following the latest market rumours in an attempt to “beat the game” against hundreds of thousands of other market participants worldwide – you can also simply chill out and take advantage of BitcoinVN’s new DCA feature: set it and forget it.

Utility of Gram (TON)

As mentioned above, Gram (TON) is one of the few coins that has seen some actual real-world traction though this comes with an important caveat:

That traction remains largely concentrated within Telegram and its surrounding ecosystem. However, Telegram itself is a very large market: over one billion users, strong distribution, and a generally developer-friendly environment that allows people to build mini-apps and integrations relatively seamlessly.

In that sense, Gram (TON) is somewhat comparable to a form of “airline miles” inside a very powerful network. It may not be the base layer of a truly decentralized financial system, but it does have utility within an ecosystem with significant reach.

As long as Telegram retains a similar level of popularity and attention, and as long as Durov and his team continue to support the project, there should likely remain ongoing demand for Gram (TON) tokens. That demand creates a persistent bid for the asset, as users need the token to perform certain transactions inside the ecosystem.

This is not entirely different from Tron, Ethereum, or other “platform tokens”. They may or may not be attractive long-term investments, but due to their widespread distribution and usage, there is ongoing market demand for their tokens because they are required to conduct specific transactions and activities within their respective ecosystems.

As for Gram (TON), some of the more notable use cases include:

- Fragment Marketplace – Telegram usernames, anonymous numbers & digital collectibles: Fragment is Telegram’s official blockchain marketplace, where users can buy and sell premium Telegram usernames, anonymous phone numbers, digital gifts, and other collectibles. Every transaction is settled on the TON blockchain, making Gram the native settlement asset for a marketplace backed by Telegram’s billion-plus user ecosystem.

- Telegram Stars settlement & creator payouts: Telegram’s creator economy is built around Telegram Stars, with eligible developers and content creators able to convert their earnings into Gram. This creates another recurring source of demand for the ecosystem’s native token.

- Transaction fees (including USDT on TON): Every transfer on the TON network – including sending USDT on TON – requires a small amount of Gram to pay network transaction fees, similar to how ETH is needed on Ethereum.

Together, these use cases create a baseline level of recurring demand for Gram inside the Telegram ecosystem – not necessarily enough to make it a great long-term investment, but enough to distinguish it from the vast majority of crypto tokens that have little practical usage beyond speculation.

Utility Alone Is Not an Investment Thesis

One of the more common mistakes investors make – and one by which countless fortunes have ultimately been squandered – is confusing utility with investment quality.

Utility, in and of itself, does not make for a great investment thesis.

A toothbrush, a tyre valve, or a light switch all provide – arguably – tremendous utility.

Yet none of them makes for a particularly compelling store of value simply because billions of people use them every day.

The same argument has repeatedly surfaced in the investment world. Silver, for example, is often promoted as a superior investment to gold because “it has more industrial uses.”

Duh.

Whether an asset is useful tells you remarkably little about whether it is scarce, monetizable, or capable of compounding purchasing power over long periods of time. Those are entirely different questions.

First of all, you generally want utility assets to remain abundant, affordable, and easily accessible. If the inputs that society depends on – whether silver, platform tokens, or even toothbrushes – suddenly became scarce luxury goods, production would inevitably suffer and the cost of downstream goods and services would rise accordingly.

Put differently, you probably do not want to live in a world where silver suddenly trades at ten times today’s price. While that might benefit existing silver holders, it would also make countless industrial processes significantly more expensive – and society as a whole would almost certainly be poorer for it.

Second, reliably preserving purchasing power over long periods of time is an extraordinarily valuable property. If Gold – or Bitcoin, for that matter – performs that function exceptionally well compared with its peer competitors (be it other metals or alternative cryptocurrencies), there is little reason to deliberately settle for the second-best alternative.

After all, while you can build wheels out of wood or stone, most people would rather use rubber tyres. When a clearly superior tool exists for a particular job, using an inferior substitute usually means accepting lower performance for greater effort.

The return of the Gram brand & the MTONGA plan by Durov

Long-time cryptocurrency users may remember that Gram was originally the name of Telegram’s planned cryptocurrency during its record-breaking 2018 token sale. That original project was ultimately halted following legal action by the U.S. Securities and Exchange Commission (SEC), leading Telegram to abandon its direct involvement while the open-source community continued development under the name The Open Network (TON).

In the years following the SEC settlement, Telegram and Durov gradually began re-engaging with the ecosystem. Rather than attempting to recreate the original ICO-era structure, Telegram instead focused on integrating the blockchain into its existing products – introducing Telegram Wallet, Mini Apps, Fragment, Telegram Stars, and USDT support – while leveraging Telegram’s distribution to drive real-world adoption.

The recent transition back towards the Gram brand appears to form part of a broader strategy to unify Telegram’s growing blockchain ecosystem under a single, consumer-friendly identity.

Beyond the rebranding itself, Durov has also floated the broader “Make TON Great Again” (MTONGA) initiative – a strategy aimed at accelerating ecosystem growth through deeper Telegram integration, expanding developer tooling, improving user onboarding, and positioning Gram as the native economic layer for Telegram’s rapidly growing digital economy. Whether every aspect of that vision ultimately materializes remains to be seen, but the direction of travel is clear: rather than building “another cryptocurrency”, Telegram increasingly appears focused on embedding blockchain functionality directly into products that hundreds of millions – and potentially over a billion – people already use.

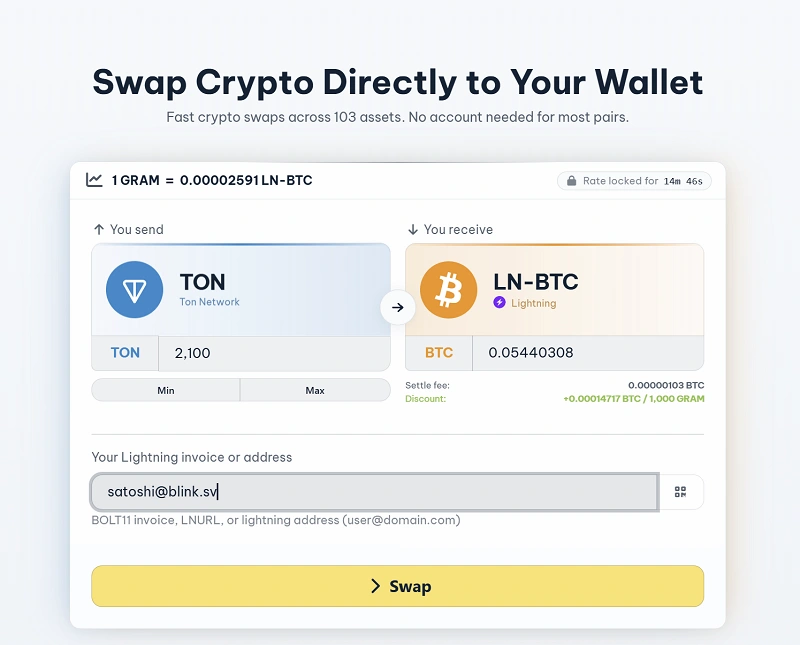

BitcoinVN infrastructure upgrades 2026 – Larger swaps & USDT on TON support

As TON – or as it is now once again known, Gram – remains, in our view, one of the more active blockchain ecosystems with significant real-world distribution, it is our responsibility – regardless of our own investment thesis – to provide fast, reliable swap infrastructure for both end users and developers building on top of the BitcoinVN Swap API.

Accordingly, we have removed the previous US$1,000 swap limit for Gram and increased the maximum instant swap size to US$100,000 per transaction.

The same upgrade now applies to USDT on the TON blockchain, allowing significantly larger instant swaps than previously possible.

USDT on TON has already become a meaningful stablecoin deployment, with USDT representing the dominant stablecoin inside the TON ecosystem. While still far smaller than the established stablecoin juggernauts such as Tron, Ethereum and Solana, TON’s integration with Telegram gives it a credible path to further growth as a settlement network for digital payments.

Given Telegram’s unparalleled distribution and Pavel Durov’s renewed focus on expanding TON as a settlement layer for digital payments, we would not be surprised to see TON continue gaining market share within the broader USDT ecosystem over the coming years.

As regular readers will know, the BitcoinVN Research team will continue monitoring these developments and publish updated analysis on this site as the ecosystem evolves.

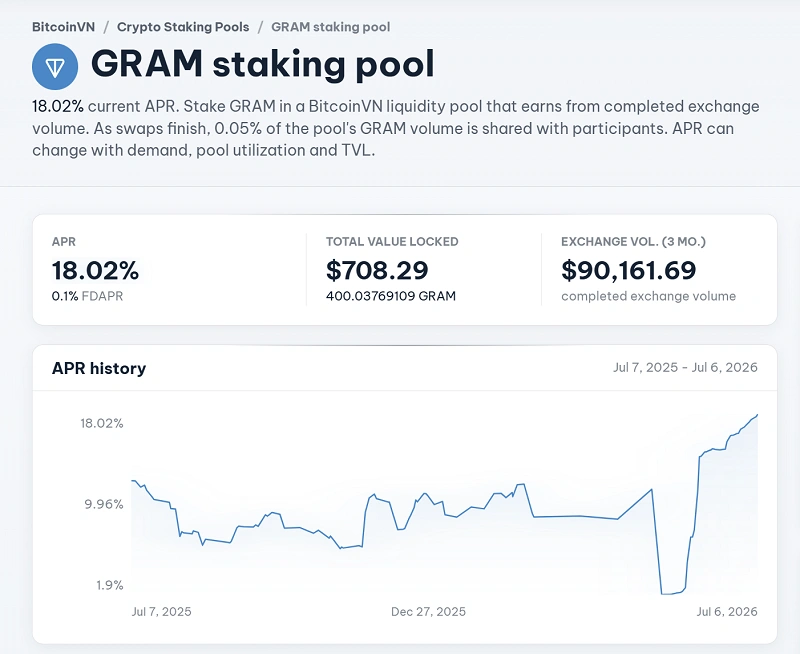

Earn Yield on Gram (TON)?

As usual when we mention it:

Yes, BitcoinVN offers a Liquidity Provider program which – by market standards – currently provides a comparatively attractive return on staked Gram (TON).

But also yes: this comes with counterparty risk. Not your keys, not your coins. An adverse incident on BitcoinVN’s side could, in an extreme case, lead to a total loss of funds.

You should only consider participating if a potential loss of the funds would not materially affect your financial situation or personal circumstances.

Liquidity provided to BitcoinVN helps maintain sufficient capacity for swap activity on the BitcoinVN platform. While no fixed APR is promised, the program can provide a relatively attractive yield to sophisticated investors as long as TON/Gram remains in reasonable demand and usage.

Self-Custody of Gram (TON)

As always, our standard recommendation for the vast majority of users remains unchanged:

Take self-custody of your assets – and eliminate unnecessary counterparty risk.

Gram (TON) can be self-custodied, but hardware-wallet support is not universal. Among the devices currently available through BitcoinVN Shop, the cleanest option is Ledger: Ledger Nano S Plus, Nano X, Ledger Flex and Ledger Stax all support Gram (TON) through the Ledger ecosystem. Keystone 3 Pro can also be used, but requires Tonkeeper as the companion wallet. Trezor, by contrast, does not currently support Gram (TON).

For users based in Vietnam, compatible devices can be purchased via BitcoinVN Shop, with same-day delivery or self-pickup available in Ho Chi Minh City and Da Nang, as well as fast nationwide shipping from our local warehouse.

If you’d like to deepen your understanding of self-custody, we publish regular cybersecurity and best-practice guides on BV Insights. Alternatively, if you’d like help getting started – or simply want an experienced second pair of eyes to review and harden your existing setup – you can book a 1:1 session with our BitcoinVN Consulting team. We can help you design a self-custody setup that matches your technical ability, risk tolerance and long-term objectives.

Integrate with BitcoinVN

If you are a developer – or otherwise looking to integrate cross-asset swap functionality into your business or application – you can review the BitcoinVN API documentation here.

We operate both our liquidity and technical infrastructure in-house, helping ensure that swaps are executed quickly, reliably, and with limited dependency on third-party providers.

BitcoinVN is one of the longest-operating digital asset firms globally, with an operating history dating back to early 2014. The company was originally founded by a mixed team of early Vietnamese Bitcoin enthusiasts, supported by European expatriates from the Frankfurt region – one of Europe’s major financial centres and a region with long-standing cooperation links to Ho Chi Minh City, Vietnam.